Seigniorage

or, The price of money

Last time, we saw that in the 1920s, the Federal Reserve adhered to a long-criticized economic theory called the real bills doctrine, which held that the Fed could constrain inflation by linking the expansion of the money supply to so-called “real bills,“ meaning short-term credit instruments for transactions involving goods and services. The theory behind the real bills doctrine was that growth in the money supply, when modulated by actual production, would support economic growth without triggering non-productive financial speculation.

Real bills

A recurring theme in my recent excavations of America’s financial history has been the perpetual banking panics that have incessantly gripped the American economic system. These periodic crises appear frequently to mark the turning point in the business cycle, whereby a rapidly expanding economy overshoots its own capacity, only to realize abruptly and …

As I described, the flaw in the real bills doctrine was that prices contained in “real” bills can change without necessarily reflecting any change in the underlying productive activity. Because an increase in the money supply automatically puts upward pressure on prices, pegging the money supply to the face value of bills creates an inflationary feedback loop between price and money supply.

I have noted elsewhere the connection between price levels and the money supply, and in particular how increasing the amount of money in the economy is inflationary (i.e. results in a general increase in prices). For example, the federal government’s first experiment with fiat currency during the Civil War was highly inflationary because it flooded the war-time economy with paper notes, called greenbacks, not backed by specie.

Greenbacks

I previously described how in the early modern era the “holder in due course” doctrine made private debt instruments negotiable, so that they circulated as mediums of exchange (paper money). In that way, they could substitute or even supplement the money supply consisting of gold and silver. Paper currency could facilitate commercial activity by amelior…

In fact, the establishment of the Federal Reserve System itself resulted in an inflationary expansion of the money supply by changing the reserve requirements of member banks. As I have previously described, banks can expand the effective supply of money in the economy, without the creation of any new physical currency, by lending their demand deposits and retaining in reserve only a fraction of their outstanding obligations, effectively double-booking the money in your checking account.

The Money Multipliers

In 1791, the United States of America was a decentralized and under-developed economic backwater. But the country’s first Treasury Secretary, Alexander Hamilton, had a plan. He intended to weild the powers of the federal government, newly granted in the recently ratified Constitution, to transform the American economy through what we would today call ec…

Hester explains that, when member banks were required to deposit their reserves in their respective regional Federal Reserve Banks, their overall reserve requirements were simultaneously reduced “to decrease the burden of membership on national banks and attract more state-chartered banks to the system.” The difference resulted in “excess reserves” burning a hole in member banks’ pockets that could be lent, thereby expanding the money supply and triggering inflation.

But why does increasing the amount of money make stuff more expensive? To answer that, first we need to understand how markets set prices for particular goods and services.

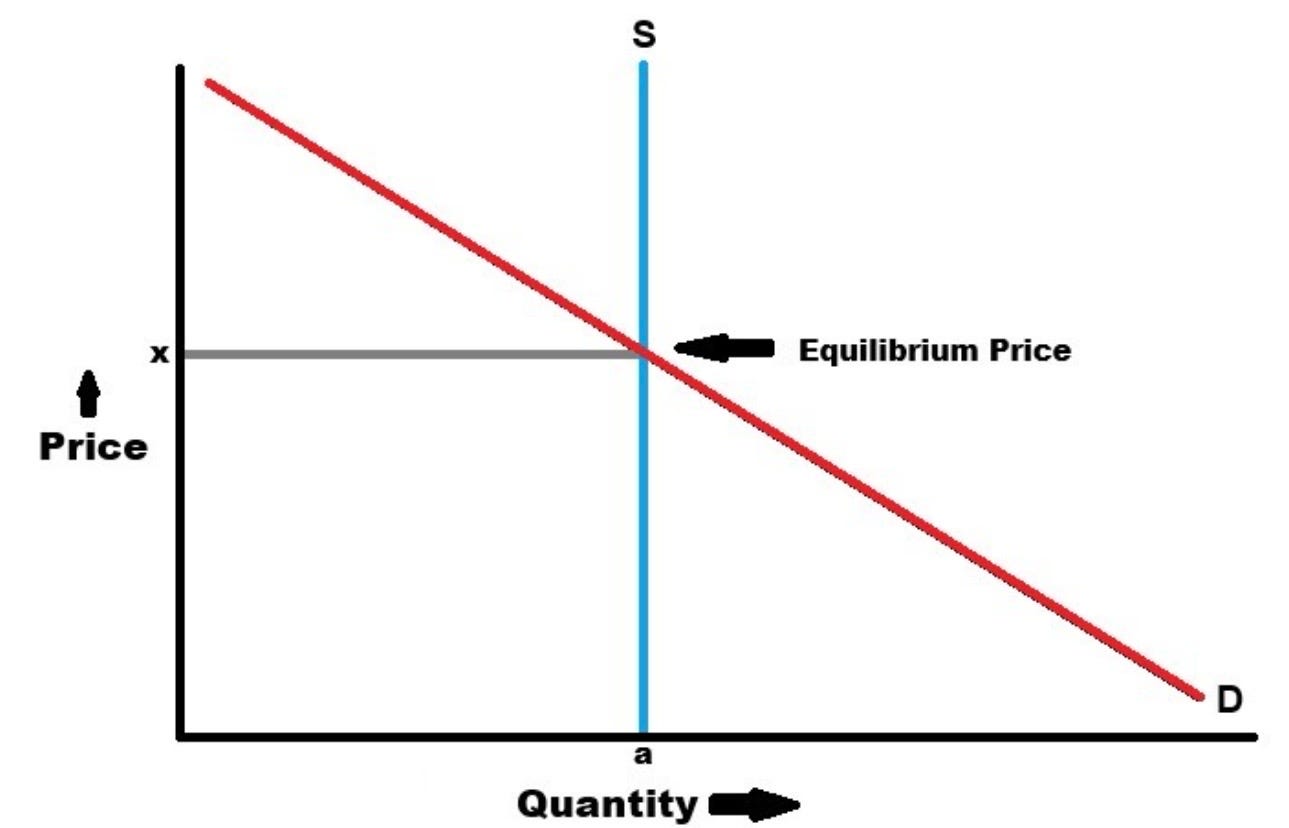

All other things being equal, the price for a given good or service that the market naturally lands on, known as the equilibrium price, depends on the supply and demand for that product. In general, the more expensive something is, the less of it consumers will want to buy, while conversely, consumers will want to buy more of it when it is cheaper. Thus, we can posit a “Law of Demand” that demand is inversely correlated with price, represented graphically as a falling “demand curve.”1

For these purposes, we can represent the supply of the product as a straight vertical line, representing the existing stock.2 Depicted graphically, the point at which the two lines meet is the equilibrium price.

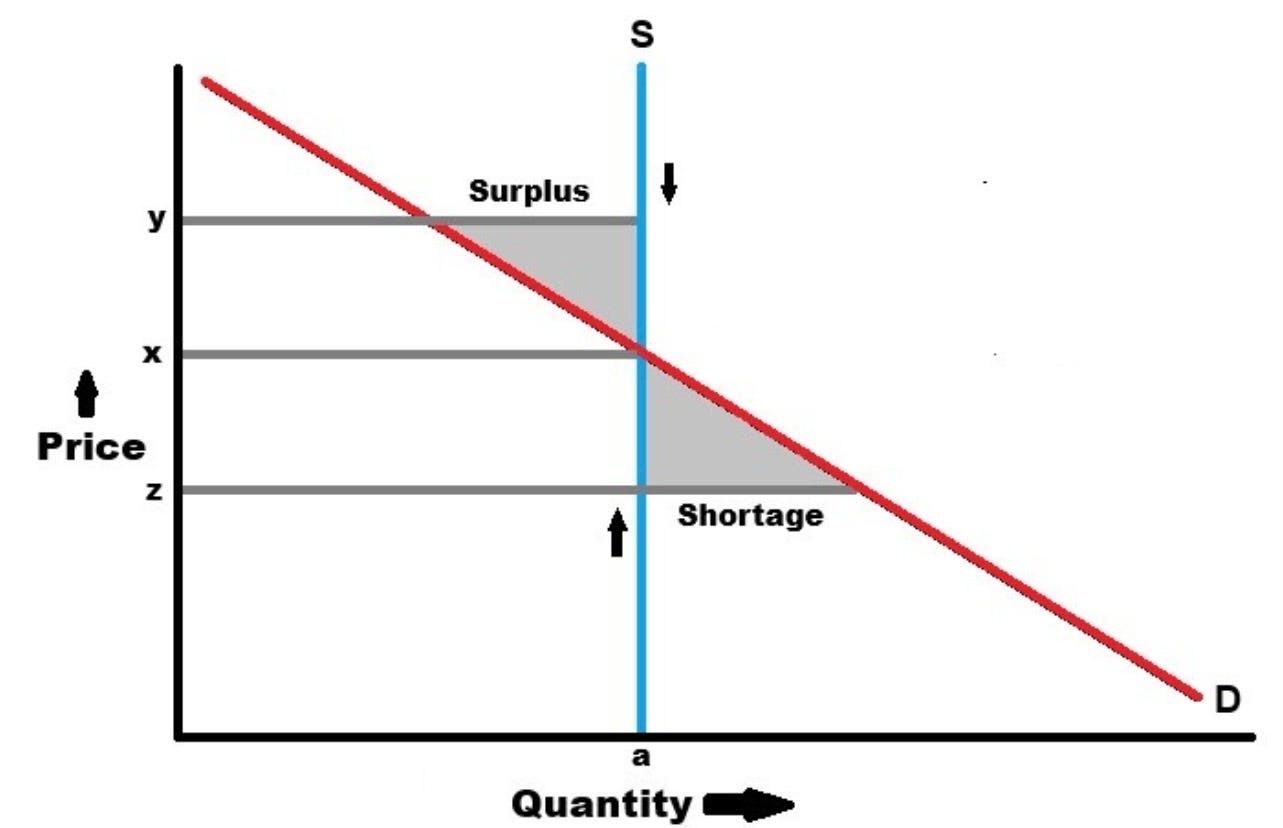

If price is set above the equilibrium price, the demand curve is below the supply at that price, resulting in an unsold surplus and market pressure to reduce the price to clear the surplus. If, on the other hand, price is set below the equilibrium price, demand exceeds supply, causing a shortage and pressure to raise prices. This is why the natural market price for a product is called the “equilibrium;” any deviation triggers counter-incentives back to the market price.

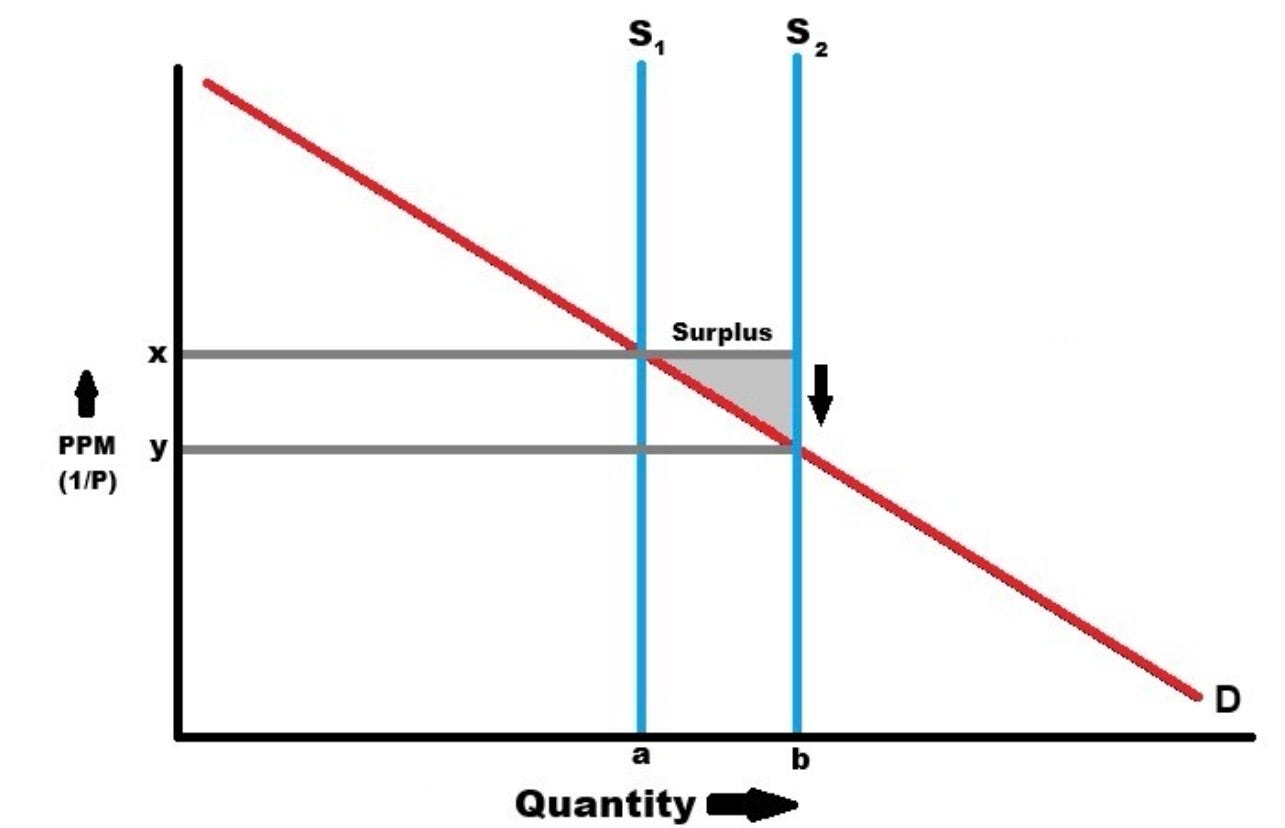

So if the price of a product should tend to remain stable, why do we in fact observe that prices rise and fall all the time? A change in the supply or demand for the product itself will produce a new equilibrium. For example, if there is a drop in supply (the supply line shifts left), a shortage occurs at the current price (there are more people willing to buy at that price than product available) and price rises until a new equilibrium is found. If demand falls (the demand curve moves down), a surplus is created at the current price (there is more product than people willing to buy it at that price), and the price falls to a new, lower equilibrium.

If prices for particular goods and services are determined by supply and demand for those particular products, why then is there inflation, a general rise in prices across the economy? One reason might be a shortage in a good that is an input for many other products. If, for example, Iran were to close the Strait of Hormuz for a sustained period of time, it would decrease the global supply of oil. Since oil is needed to produce essentially every other product, an increase in the price of oil resulting from the shortage will drive up the prices of everything else.

But, in addition, as we have seen, an increase in the supply of money itself can impact overall prices and lead to inflation.

The supply of money

It may feel counter-intuitive, but money itself can be thought of in terms of a dynamic involving supply and demand similar to that for goods and services just described. By doing so, we start to see how increasing the amount of money in the economy might produce inflation.

First: the supply of money. In the days of yore, when money consisted mainly of specie, the supply of money was just the total amount of gold, silver, or other precious metal held by all the participants in the economy.

You might think that in such a metal money regime, the government would lack the ability to easily expand the money supply. To get more gold, the government would need to either dig it out of the ground or obtain it from someone else, through trade or plunder.

But even when money was just gold, governments got involved in the money supply by minting coins. Coinage was very useful for facilitating exchange, because it provided standard units of specie in predetermined amounts. Thus, a seller would know exactly how much gold she was receiving in any given transaction, without having to resort to an a metallurgist each time.

But an odd side effect of unit-ifying commodity money is legally divorcing the underlying commodity from the unit of exchange. The British Pound, for example, once upon a time was actually a weight of silver. But over time, the “Pound” became an abstract concept, rather than a literal weight of metal.

The government could take advantage of the distinction by debasing the coinage through what were called seigniorage fees. When you went to the royal mint to coin your pound of silver, the government retained a portion of it as a fee for the privilege, say 1/10th.3

Now your “Pound” was really only 9/10s of a pound. But as legal tender, it was still a fully-fledged English Pound. And, after minting nine Pounds, the government had collected enough silver in seigniorage fees to mint a new 9/10ths “Pound“ of its own. Thus, through seigniorage, the government could make money for itself and expand the money supply at the same time.

Of course, in the modern times, money is no longer primarily a matter of precious metal. In our new conception “relevant only since the 19th century,” Benjamin Friedman writes, “money is a form of debt.” But although paper money began as bills memorializing financial obligations, originally between private parties and then later of the government itself, the concept has in practice become totally abstracted from negotiable debt instruments.

Fat Stacks: An Origin Story

Over the last few posts, I have been interested the early history of American monetary policy, a supremely obscure topic, to be sure. Last time, I asked, what’s the deal with money, anyway?

Modern fiat currency does not bear interest and “although it is the government’s (the central bank’s) liability, in modern times it usually does not represent an obligation on the government’s part to pay the bearer in some other form.” Rather, “both private citizens and businesses hold these government liabilities for their convenient use in everyday transactions, normally enforced by their statutory status as legal tender.”

Unlike in the case of specie, the government’s capacity to expand the supply of fiat currency is essentially limitless. The government can, of course, cheaply produce endless supplies of paper bills, but the printing of physical cash is not the primary way that the US government creates new money. This is because the “money that individuals and firms use mostly consists of deposits issued by banks and other financial institutions.”

As we have seen, under the fractional reserve system of banking, the money you have in your checking account is not reflected by an actual equivalent quantity of cash in the bank’s vault. Rather, the bank only holds a fraction of the money on its books as actual cash and can ”increase” the amount of your deposits by merely changing ledger entries in their accounting system. Since the ratio between the amount of outstanding money the bank has “created” and the cash reserves backing it up is set by the government, the government can manipulate the amount of money in the economy indirectly by altering banks‘ reserves.

The supply of money in the economy, then, is the total amount of money held by all the individuals and firms in the economy, including both cash and deposits. It’s expressed mathematically like this, where M is the total supply, m is the amount owned by each individual or firm, and ∑ is the sum of the ms:

M = ∑m

The demand for money

You might think that the demand for money is just, “all the money.” Who doesn’t want more money, right?

But when economists talk about the demand for money, they mean the amount of available cash people want to hold onto, instead of spending or investing it. In that sense, the demand for money is not unlimited. And just like demand for goods and services, the demand for money depends on its price.

But what is the “price” of money? In monetary theory, the price of money is often said to be the inverse of the general level of prices. In other words, it is money’s purchasing power, or how much stuff you can buy with it.

That seems weird at first, but it makes sense if you think about it like a barter exchange. If you trade me your coconut for my melon, the “price“ of your coconut was one melon, since I ”bought” your coconut by paying you a melon.

Similarly with money, when you buy things with money, the other person is paying you for your money with goods and services. So if I bought your coconut for $5, you paid me a coconut in exchange for $5 (the price of $5 was a coconut). We don’t calculate the price of money in coconuts, obviously, but from that idea is derived the proposition that the price of money is it’s purchasing power (how much stuff you can get for your money).

That the purchasing power of money is the inverse of the prices of goods and services also makes sense because the more expensive goods and services are, the less you can buy with the same money and vice versa. Now, it follows that the lower the price/purchasing power of money is (i.e. the more expensive stuff is) the more cash balances people want to hold (the higher the demand for money) because they anticipate needing more money to buy things.

Thus, the demand curve for money slopes down just like the demand curve for other things we saw above. And the place where the demand curve for money crosses the supply is again, the equilibrium price of money.

So what happens when the government increases the amount of money? There is now a surplus of money (more than is demanded at that price). Since people now have more money than they anticipate needing to hold onto, they spend that surplus on goods and services, driving up the demand for those products and in the process, the prices for them as well.

Because the price of money is the inverse of the general price level, an increase in the prices of goods and services is the same as a decrease in the price of money. Money is now worth less and you cannot buy as much with the same amount of money that you could before the increase in the money supply.

In theory, if the government could simultaneously increase the amount of money proportionally across the entire economy, it would have no real impact at all. Prices might be twice as high, but you’d have twice as much money, so it would be a wash. That is sometimes referred to as the “neutrality” of money.

Perhaps money is neutral over the long run, but in practice sudden changes in the money supply have significant economic impacts in the near term. For one thing, not all prices rise simultaneously at the same rate in response to an increase in the amount of money. Some prices are “sticky,” meaning that they are slow to respond to changing conditions.

Wages, for example, are notoriously sticky (wages are the price of labor). While economists tend to focus on the “downward rigidity” of wages, we have all had the sense in recent years how much faster than wages prices for consumer goods can rise.

In addition, when the government adds to the money supply, it does not simultaneously increase it proportionally across the economy. Instead, it injects the money at certain points to the benefit of certain market participants and not others, creating winners and losers in the process.

The biggest winner, of course, can be government itself. The biggest losers, on the other hand, are typically average Joes; particularly and perversely those on fixed incomes like the elderly and those who have prudently stayed out of debt and built savings.

The government can, of course, spend the money that it creates directly on goods and services, a technique that economists consider a modern form of seigniorage. According to Tobin, however, “[i]n the United States today seigniorage is a minor source of revenue,” because fiscal policy has been mostly decoupled from monetary policy.

Instead, the Federal Reserve regulates the money supply by manipulation of financial markets through occult practices like open market operations. On the other hand, “for many less developed countries printing money is a major way of financing public expenditures; seigniorage is a major source of revenue, because implicit taxation by inflation is politically easier than explicit taxation.”

Nevertheless, as I have said before, inflation is a boon for debtors, because they end up paying back the debt in cheaper dollars than they borrowed. Inflation decreases the principal of the debt in real terms. Creditors conversely, loose out by inflation because they are paid back in money that is worth less than that which they lent.

Bimetallism

We saw last time that, in response to the financial necessities of the Civil War, the federal government issued the first ever true fiat currency in American history, colloquially known as “greenbacks.” These were technically a type of Treasury notes, nominally negotiable debt instruments, but in fact not redeemable for gold or silver by the government.…

The national government is no exception to this dynamic, but is in a unique position to influence the rate of inflation, and in effect, reduce its real debt level. But inflation simultaneously erodes the purchasing power of ordinary people’s savings and incomes. For this reason, some economists consider inflation an insidious, hidden form of taxation.

Inexplicably, economists depict the demand “curve” with a straight line.

Since a rising price will induce producers to increase supply, the supply “curve” can be depicted as a rising slope (there is a direct relationship between price and quantity supplied).

In reality, of course, a pound of silver would have made an unwieldy coin. The pound was divided into 240 pence.