Bimetallism

or, The gold standard and its discontents

We saw last time that, in response to the financial necessities of the Civil War, the federal government issued the first ever true fiat currency in American history, colloquially known as “greenbacks.” These were technically a type of Treasury notes, nominally negotiable debt instruments, but in fact not redeemable for gold or silver by the government. By the end of the war, something like a half a billion dollars worth of greenbacks were circulating in the American economy.

Greenbacks

I previously described how in the early modern era the “holder in due course” doctrine made private debt instruments negotiable, so that they circulated as mediums of exchange (paper money). In that way, they could substitute or even supplement the money supply consisting of gold and silver. Paper currency could facilitate commercial activity by amelior…

When the constitutionality of the currency was subsequently challenged in Hepburn v. Griswold (1869), the U.S. Supreme Court had initially held that greenbacks could not be required legal tender for debts incurred prior to enactment of the Legal Tender Act establishing them. This was very bad news for anyone who owed money on a debt incurred prior to the war, including many railroad companies, because they would now be required to repay their debts in specie instead of paper.

In a case of what we might today characterize as court-packing, the Republican dominated Congress expanded the number of justices on the Court, giving President Grant an opportunity to appoint two ex-railroad lawyers to the Court. The Court duly performed an abrupt volte face in Knox v. Lee and Parker v. Davis (1870), upholding greenbacks as a necessary and proper measure to sustain the war effort.

Nor was fiat currency Congress’s only innovative fiscal move to sustain the war effort. They also established the National Banking System, which involved a series of nationally chartered banks overseen by a federal comptroller. These were private for-profit institutions, but the assertion of federal control over the banking industry nevertheless primed the pump for the later institution of the federal reserve system in the twentieth century.

The National Banking System consisted of three tiers of federally-chartered banks: central reserve city (located only in New York), reserve city (for other cities with populations greater than 500,000), and country banks. Although these national banks were required by federal law to keep certain amounts of reserves on hand, these reserves could be held in any lawful currency (and not just precious metals). In addition, reserve city banks could maintain some reserves as demand deposits in central reserve city banks, and country banks could maintain reserves as demand deposits in both central reserve and reserve city banks.

The point of the new national banks from the federal government’s point of view was that they would buy war bonds. Since the banks’ reserve requirements needed not be held as specie, they could instead be tied in part to the amount of Treasury bonds the banks maintained, meaning that if they wanted to expand their business, they would buy federal securities. Thus, the federal government generated a captured market for its war-finance.

At the same time, Congress enacted an onerous tax on state bank notes, in an effort to drive them out of circulation. Although state banks were initially devastated by the hit to their business model, they eventually bounced back once they realized they could hold their reserves in the form of greenbacks, federal bank notes, and demand deposits in national banks, relieving them of the need to hang onto so much scarce bullion. They essentially joined the National Banking System by opening demand deposits with the national banks to hold their “reserves” of federal paper.

But not everyone was happy with the new order. Advocates of so-called “hard money” wanted a gold standard, meaning that every piece of paper currency in circulation should reflect an actual equivalent amount of gold sitting in the U.S. Treasury.

These goldbugs were appalled by the inverted pyramid of paper money created by greenbacks and the National Banking System: state bank demand deposit accounts based on national bank notes, based on greenbacks, based on nothing more than the reputation of the federal government. According to these hard-money advocates, it was expansionary monetary policy, especially fiat currency, that was to blame for inflation and the boom/bust economic cycle.

The Crime of ‘73

As I have written, with the Mint Act (aka the Coinage Act) of 1792, Congress had established the U.S. Mint and designated the dollar as the national unit of currency. Alexander Hamilton, whose brainchild the Mint Act was, had recommended the adoption of “bimetallism,” meaning that both gold and silver would be minted into dollars, “in order not to abridge the quantity of circulating medium.” Thus, the Mint Act provided for both gold and silver dollar coinage and specified defined quantities of metal for each.

Mediums of exchange

In the early years of the American republic, the national government lacked a firm control over the circulation of money in the economy and in fact initially did not possess exclusive power to coin money. During the Confederation period, individual states could also strike their own coins and experiment with paper tender.

What might seem wild to a modern reader is that the Mint in that era did not coin money from reserves of precious metals held by the government itself. The early federal government was cash-strapped in the extreme and was otherwise preoccupied in experimenting with a central bank as a desperate gambit to expand its access to paper money in the form of federal bank notes. Instead, the Mint accepted deposits of bullion from citizens, struck them into coins, and then returned the specie to the depositors in the form of gold and silver federal dollars.

The flaw in this system was that the relative market value of gold and silver fluctuated over time, while the legally defined specie-content of coins did not keep up. When the commodity value of gold or silver contained in a coin exceeded its face value, people hoarded the coins or traded them on foreign markets, which resulted in a drain of specie overseas. By the time of the Civil War, for example, debasement of the gold dollar by Congress in 1834 combined with a glut of gold from California and Australia had chased silver dollars out of circulation (foreign silver coins continued to circulate, however).

Congress of course exploded this whole paradigm with the Legal Tender Act of 1862, by establishing paper fiat currency as legal tender in the form of greenbacks, which were irredeemable in either gold or silver and did not earn interest (unlike pre-war Treasury notes). In the wake of the Civil War, Richard White writes in The Republic For Which It Stands, currency in the form of specie was “nominal because dollar denomination coins were so scarce as to be invisible in ordinary transactions.”

But Democrats and, increasingly, conservative-leaning Republicans were deeply disturbed by this brave new world of fiat currency based on nothing more than the government’s full faith and credit. They “considered only currency redeemable in gold as real money - so-called hard money[:]”

The more wealth became a matter of paper - stocks, bonds, and bank checks - the more liberals fetishized gold. It was rare, could not be reproduced and held its value. Paper, on the other hand, could, like Confederate currency or the stocks and bonds of failed companies, seem a fortune one day and end up as the lining of trunks the next. Paper threatened to render the world flimsy, ephemeral, and open to constant negotiation, which made it all the more necessary that order be restored and all value be reducible to gold.

While the “debate over monetary policy often seemed more theological than political,” opposition to paper money was not only a matter of vibes. Gold standard advocates argued that unconstrained expansion of the money supply through paper notes caused inflation. In addition, moving to the gold standard would facilitate foreign exchange and commerce and provide more favorable terms for obtaining foreign credit.

But even if hard money men felt that the value of gold was somehow intrinsic to the metal itself, the gold standard “was neither ancient nor natural.” It was as new as the fiat currency system that made it salient.

Indeed, the United States, as we have seen, had been bimetallist right from the jump, even setting aside the voluminous private paper instruments circulating effectively as currency (backed only on a fractional basis by specie). It was Great Britain that first adopted the gold standard in 1819, but it took another 40 years for other countries to start following suit.

Nor would a transition to the gold standard be painless. It would require a significant reduction in the amount of circulating currency, since every greenback would have to be redeemable for gold. Such a monetary contraction would almost inevitably involve a corresponding economic contraction involving deflation, unemployment and bankruptcies.

In addition, adoption of the gold standard would “remove[] control of the financial system from the United States to London, the seat of the international economy and capital of the world’s creditor nation.” Finally, in combination with the National Banking System, hard money would exacerbate the concentration of wealth and financial power in the Northeast, leaving the South and West credit and cash starved.

But like Lord Farquaad, those were sacrifices the Eastern financial class was willing to make. Deflation would, of course, mean that their cash wealth would be worth even more in terms of purchasing power. Banks and bondholders were enthusiasts of hard money, because it meant that the dollars they would be payed back in would be worth more in real terms than those which they had originally lent out. Conversely, as usual, the poor and indebted would need to take one for the team.

The proponents of gold struck first against bimetallism with the Coinage Act of 1873, which effectively demonetized silver domestically by eliminating the silver dollar. At the time of its passage, the measure was little remarked upon, because enthusiasts of fiat currency regarded silver as just another type of specie and failed to recognize its expansionary potential (the price of silver was dropping with the discovery of the Comstock Lode, making silver more attractive vis-a-vis gold as coinage).

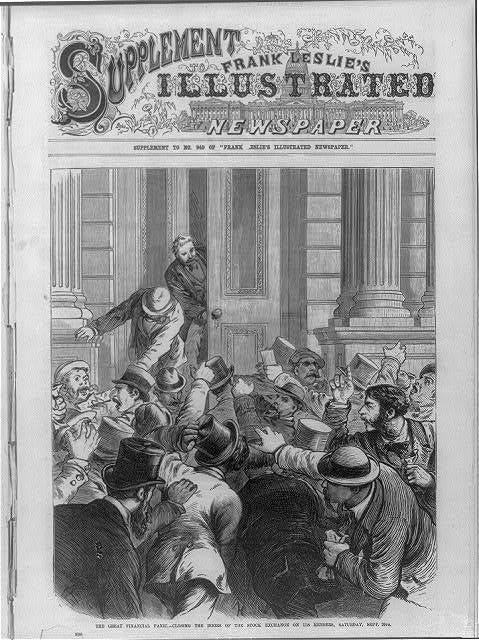

Then came the Panic of 1873, a financial crisis brought on in large part by railroad speculation. The Panic was triggered when the New York branch of the Jay Cooke & Company bank suddenly went under after being unable to market its railroad bonds. The New York Stock Exchange closed its doors for the first time ever, “[b]anks called in loans, businesses collapsed, and the United States slid into a depression, which would last until 1879.”

Only too late did “antimonopolists and soft-money men recognize[] silver as the inflationary option to the gold standard in a deflationary would.” In retrospect they lamented the Coinage Act as the “Crime of ‘73” and “lay responsibility at the feet of Eastern and European bankers.”

But hard money men saw inflationary fiat money as the root cause of the financial crisis. They doubled down with the Specie Payment Resumption Act of 1875, which required the Secretary of the Treasury to redeem greenbacks in gold on demand beginning in 1879. Nevertheless, the law was not a total victory for the gold standard, since it did not provide a mechanism for the government to acquire the gold necessary to redeem the circulating paper.

The People’s Party

The credit and cash crunch that followed the Panic of 1873 fell particularly hard farmers, who depended on debt. Farmers responded to deflation by increasing production to make up the difference, which only exacerbated falling commodity prices by flooding the market. Deflation in turn meant that farmers had to pay back cheap dollars they borrowed with more expensive deflated dollars.

The Catch-22 was particularly acute for Southern cotton producers, who were caught in the crop-lien system. Under this paradigm, unplanted cotton could be liened, so that the future cotton crops served as collateral for credit to fund its planting. Although Southern legislatures had enacted crop-lien legislation with good intentions, writes White, “they saddled the South with a [...] system that would burden the region for generations.”

As impoverished cotton sharecroppers became increasingly leveraged,

[t]he various lien holders battled in court when the crop was short and could not cover all debts. Store owners who advanced goods on credit took their own merchandise on credit from wholesalers who [...] in turn, depended on credit advanced them by northern manufacturers or money borrowed from northern banks. Everything ran on cotton and credit. The Southern economy rose and fell with the worldwide demand for the crop. Rising cotton prices meant more cotton, but so too did falling prices, which necessitated more cotton to cover debts. Debt, credit, and cotton marched together across the South.

The Panic of 1873 was also a total catastrophe for the Grant Administration that broke the monopoly on federal power enjoyed by the Republican Party since the end of the Civil War. It also fractured the party, with some soft-money Republicans jumping ship for the new, independent Greenback Party. The Panic “undercut both Republicans and moderate Democrats and fed a resurgent white supremacy” that “became the glue that held the Democratic Party together.”

The Greenback Party was a flash in the pan, but in its wake arose the Populist Party. It emerged from the Farmers’ Alliance, a national agrarian movement that sought to protect small farmers against the monopolistic grip of corporate power. The Populist Party agitated for collective bargaining, greenbacks, federal regulation of railroads, a progressive income tax, direct election of senators, an end to corporate subsidies, secret-ballot elections, a shorter workweek and workday, and a “Sub-Treasury” system to replace the crop-lien system.

Charles Postel explains that

[n]ever in history had rural Americans been so organized or so determined to improve their position within the commercial and social order. Officially, the Farmers’ Alliance and similar groups were non-partisan and worked for reform through the existing parties. But when that policy failed, by the early 1890s many farm reformers took the fateful step of building an independent, third party movement. The Populist Party rose on the shoulders of the Farmers’ Alliance and the organized power of American farmers.

Bimetallism became a major plank of the Populist reform agenda. They supported expanding the monetary supply and lowering interest rates. Professor White notes that at this point, oddly, “fiat currency lost ground to various proposals for silver.”

The obsession with gold was criticized as an “ancient superstition” because gold is really just a shiny metal and has no more intrinsic value than anything else. But “silver advocates essentially attacked the nearly religious worship of gold by proposing another metallic deity - silver - which could also claim ancient lineage.” Its main advantage was that, in the late nineteenth century, it was far more abundant than gold.

Gold standard advocates, meanwhile, “associated gold with stability, natural values, a hormony of interests, prosperity, civilization, the white race, expertise, and American participation in the international economy” based in London. Silver, on the other hand, was the currency of China, India, the South American republics, and other barbarian nations. But hard money men had no answers for the plight of ordinary farmers trapped in the crop-lien system.

The Populist Party made a big splash in the election of 1892, winning the governorships of Colorado, Kansas, and North Dakota and gaining control of legislatures in California, North Carolina, and other states. But the Populist political movement faced the same challenges that have stymied third parties through American history, as Postel describes:

To the extent that they appealed to voters against partisan politics, they undercut their own ability to conduct political warfare. And everywhere the realities of the winner-take-all political system worked against the success of a third party. In the Northeastern states, powerful Republican and Democratic machines effectively froze out a Populist challenge. Elsewhere, when the two traditional parties faced each other in competitive elections, one of the parties would adopt reforms attractive to Populist-minded voters, again freezing out the third party.

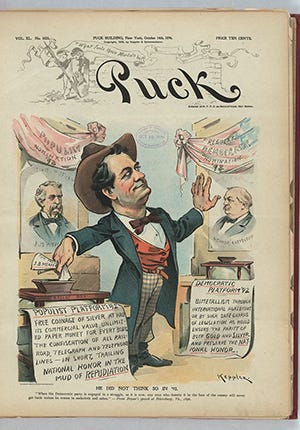

Following that playbook in 1896, Nebraska Congressman William Jennings Bryan stole the Populists’ thunder with his Cross of Gold address attacking the gold standard and calling for “free silver” at the Democratic National Convention. His speech advocating bimetallism, still regarded today as one of the greatest in American history, won him the nomination as the youngest presidential candidate ever at the age of 36. Bryan went on to lose to Republican William McKinley in the brutal election of 1896.

According to Postel, “Bryan’s nomination split the People’s Party, as some Populists wanted ’fusion’ with the Democratic ticket while ’middle of the road’ Populists wanted an independent People’s Party ticket.” Bryan’s subsequent loss to McKinley “proved a mortal blow to the People’s Party from which it never recovered.”

The bimetallists meanwhile had struck back against gold with the Bland-Allison Act of 1878, which brought back the silver dollar. President Hayes had vetoed the bill, but Congress was able to override the veto and enact the law anyway. They followed with the Sherman Silver Purchase Act of 1890, which required the federal government to purchase silver on an ongoing basis.

Nussbaum argues that the “increasing business prosperity of the country helped it withstand this silver load, kept within reasonable bounds by the upright and fearless efforts of President Cleveland.” In any event, this “dangerous silver purchase policy was abandoned after the failure of the famous free silver Presidential campaign of William Jennings Bryan in 1896.”

It was the Gold Standard Act of 1900 that finally put the nail in the coffin of bimetallism. The Act provided for the redemption of Treasury notes in only gold at a legally determined dollar value. The law directed that “all forms of money issued or coined in the United States shall be maintained at a parity of value with this [gold] standard, and it shall be the duty of the Secretary of the Treasury to maintain such parity.”

Bimetallism was vanquished and the United States was set firmly on the gold standard in 1900. But it was not destined to last.